Written By

Written By

Happy Returns

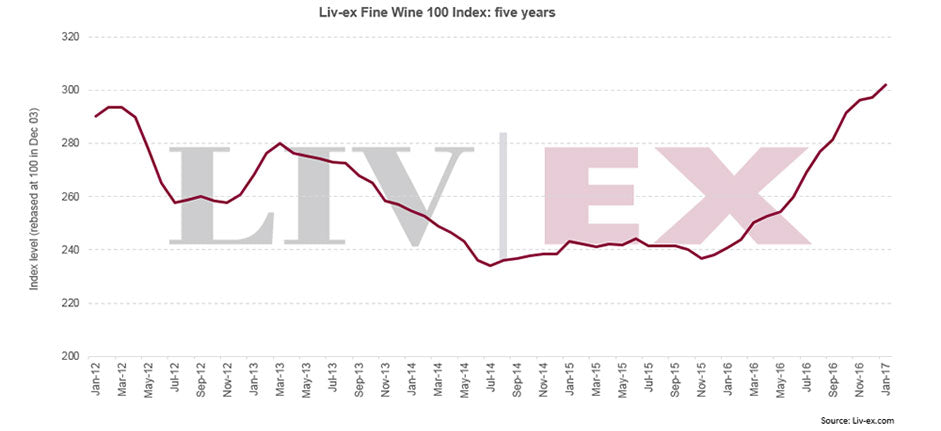

The final quarter of 2016 was a tale of two halves: a flying start with a slower finish. Whilst the trading impetus from sterling’s woes following the Brexit vote was still keenly felt in October and November, by December there was a perceptible slowdown in activity, above what might usually be expected. However, this is not to understate the remarkable performance of the market over the course of the year.

Having closed in November 2015 at 237, perilously close to the five year low (234 in July 2014), six months later the index closed the end of May over 7% up at 254. Having weathered the full force of Brexit over the second half of the year, the index closed 2016 at 297, up 24.8%. Not fully negating the losses of the previous six years but certainly making up most of the lost ground.

It is worth remembering that the end of 2010 witnessed the peak of the Asian led bull market; during which Lafite Rothschild, depending on the particular vintage, commanded an eye watering price (£12,000 for the 2005 which currently sits at £7,600 and £21,000 for the 2000 which is now at £14,000). Lafite aside, the fact that the market is again approaching a similar level suggests a discreet but nonetheless real return of confidence. It remains to be seen whether the pause in December can be attributed to a seasonal lull or more deep-rooted concerns about the global economy.

Burgundy 2015

January brings the latest Burgundy en primeur releases and this year has seen unprecedented demand for wines across the board. Invariably the better known producers in the most favoured appellations are oversubscribed but this year demand has spread the breadth and depth of the Côte d’Or. Rightly so, quite simply 2015 is a great Burgundy vintage. Pinot Noir has taken the laurels but the whites were not overlooked. If you have not already considered 2015, now is the time to act, though be forewarned much has sold out!

Global demand for Burgundy shows no sign of abating and, with reduced yields still casting a long shadow over production volumes, supply remains squeezed. Unfortunately, 2016 offers no respite. A combination of frost and hail over the course of the growing season saw some domaines lose sizeable portions of their crop and whilst the quality is high, production levels will be low. With this in mind it is perhaps no surprise that buyers are increasingly focusing on Burgundy back vintages to sate their appetite.

Bordeaux 2016 et al

No sooner does the dust settle on 2015 Burgundy than attention will return to Bordeaux and there is much to look forward to. A successful Bordeaux en primeur campaign has the ability to inject momentum into the market, and happily it is in far more robust health than this time last year. 2015 Bordeaux was broadly well received, prices for the most part falling within buyers’ expectations though there were a few exceptions.

Early reports suggest that 2016 has produced another good to great collection of wines, châteaux owners cautiously mentioning it in the same breath as some of the great vintages of the past. How this might translate into prices remains to be seen and whilst merchants’ demands for a return to prices of old are unrealistic, so too are overly ambitious release prices. Collectors’ affection for Bordeaux may not have dwindled but the depth of their pockets has been tested over recent years. A campaign where the wines command the headlines rather than the prices would be just the tonic.

Looking ahead

Already 2017 has proffered much to comment on politically and economically and without question the wine market will be tested by these new headwinds in the coming months. It may be that the recent upturn is short lived but for the moment the market finds itself in the best of health.

Toby Herbertson