Written By

Written By

The first three months of the year have witnessed steady growth in the fine wine market.

January, often thought to be a quieter month because of (short lived) resolutions of abstinence, got off to a flyer with 2015 Burgundy proving a great success. This was helped along by last minute overseas’ orders for Chinese New Year: both Lafite and Mouton Rothschild holding drinkers’ attention. In general well priced stock was in demand, a combination of an opportunity to restock and favourable exchange rates both contributing to buyer confidence.

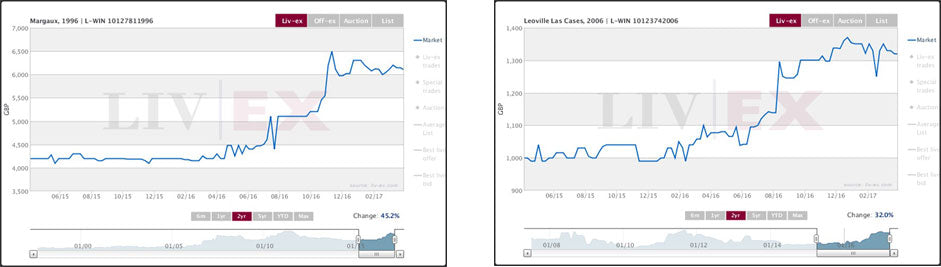

The Ch Margaux 1996 and Ch Léoville Las Cases 2006 below illustrate a fairly typical pattern for the last two years.

Whilst the dramatic recovery of the market in the six months following the Brexit vote slowed a touch in the first quarter, the Liv-ex 100 has now posted sixteen consecutive months of positive returns. Under normal circumstances this might just be a cause for concern, if based on nothing more than ‘what goes up, must come down (at some point)’. However, the start of this bull market was from a deep-set market malaise and evidently there was plenty of headroom for the market to grow into. It would now appear the market has absorbed the recent political and economic upheavals and found a strong footing. This coupled with a promising 2016 Bordeaux en primeur campaign bodes well for the remainder of the year.

Burgundy 2015

The most recent vintage release from Burgundy amply demonstrated that demand for these wines shows no sign of abating despite some higher release prices. Burgundy will always steal a march on Bordeaux due to the differing production quantities: the region produces approximately a fifth of the amount of wine that Bordeaux does and, put simply, there is not enough vin (grand cru or otherwise) to satisfy demand.

The pressure on supply has been compounded in recent years by some frankly appalling luck with the weather. Frost and hail have repeatedly blighted various vineyards the length of the Côte d’Or to the extent that from 2011 to 2013, Burgundian producers lost the equivalent of an entire harvest to inclement conditions. With restricted yields and evermore enquiring merchants it was unavoidable that there would be some modest price increases but happily, producers tried to keep them reasonable.

One dynamic Burgundy does share with Bordeaux in terms of pricing is the opportunities that present themselves in the secondary market. Comparing vintages of similar quality highlights the discrepancies that savvy buyers are taking advantage of. With buyers from all corners now competing for wines from the best domaines and production levels down, Burgundy remains in rude health.

Bordeaux 2016

This time last year the critics were lining up to heap praise on the upcoming 2015 releases. There was, it must be said, some discord as to exactly where the very best wines were produced but overall 2015 was a vintage not to be missed. Currency woes were preying on the mind of merchants as the Brexit vote loomed large.

Fast forward a year and we find ourselves in a remarkably similar situation. Currency concerns remain as Article 50 is invoked, by which the United Kingdom formally begins its exit from the European Union, and the 2016 wines are already receiving high praise.

James Suckling, a critic always quick off the mark, has released his notes and scores, stating ‘that 2016 is an exceptional vintage equal to the exquisite 2015. In some regions…the wines are even better.”

Goedhuis & Company has been reporting the thoughts of our tasting team from Bordeaux on our blog this week and our full report will be published after a second visit in a few weeks’ time.

With a larger harvest than Bordeaux has enjoyed for some time and high quality wines reportedly in many communes, it would seem 2016 en primeur is an opportunity for Bordeaux to continue re-engaging with its consumers. Whether the individual châteaux take the opportunity remains to be seen, but now all eyes turn to Bordeaux.